Summer Certification Limited Time 70% Discount Offer - Ends in 0d 00h 00m 00s - Coupon code = getmirror

Pass the CIMA Strategic CS3 Questions and answers with ExamsMirror

Exam CS3 Premium Access

View all detail and faqs for the CS3 exam

757 Students Passed

94% Average Score

96% Same Questions

A month later, you receive the following email:

Reference Material:

From: Hesham El-Sayed. Independent Non-executive

Director

To: Romuald Marek. Chief Finance Officer

Subject: Collapse of fuel supplier

Hi Romuald

I am writing to give you some advance notice of an internal audit investigation that has been commissioned by the Audit Committee

Just over a year ago. Planejoos, a newly formed company, approached the management team at Airfield's Capital City International (CCI) airport and offered to take over refueling operations at Starport Planejoos offered a higher percentage of revenue than the existing supplier was paying CCI's management team agreed and appointed Planejoos rather than renew the existing supplier's contract.

CCI was unable to conduct the usual background and credit checks on Planejoos for two reasons. Firstly, Planejoos was a new company and so did not have an extensive credit history that could be checked Secondly CCI was under time pressure to reach a decision on whether to renew the existing supplier's contract or allow it to expire

CCI's management team claimed that it had acted quickly in order to benefit from the additional revenue that could be earned from dealing with Planejoos The management team was acting on the basis that it had an ethical duty to maximise the wealth of Airfield's shareholders and that maximising revenues from fuel sales through this agreement with Planejoos was consistent with that ethical duty.

Unfortunately, as a new company. Planejoos struggled to obtain trade credit and the high demand for fuel put the company's cash flows under extreme pressure Receipts from sales lagged behind payments for inventory Planejoos has now collapsed, leaving a large trade receivable that CCI will have to write off as uncollectable CCI had permitted this receivable to accumulate rather

than pressing for payment and so putting Planejoos under further pressure.

Fortunately, the previous fuel supplier was prepared to return to CCI.

Kind regards

Hello

I have attached a news article

Arrfield does not set the price for aviation fuel sold at our airports, but we do receive a percentage of the revenues earned by the fuel companies.

I need your help to prepare for a Board meeting to discuss this matter Please write a paper covering the following

* Firstly, explain the impact that the criticisms voiced by the environmental campaigners will have on the frequent PESTEL analysis that Arrfield's Board conducts.

[sub-task (a) = 34%

* Secondly, evaluate the commercial logic of Arrfield's strategy of basing charges for non-aeronautical services (such as fuel sales and retail activities) on percentages of the revenues generated by the companies that operate at its airports

[sub-task (b) = 33%)

* Thirdly, recommend with reasons whether Arrfield should attempt to justify strategic decisions to its shareholders when the commercial logic of those decisions is not immediately obvious

[sub-task (c) = 33%}

Thanks

Romuald Marek

Chief Finance Officer

A week later, Romuald Marek stops by your workspace and hands you a document.

The Board minute extract from Romuald can be viewed by clicking the Reference Material button above.

Reference Material

Board minutes extract: proposal to profit from ongoing strength of NS

Anna Obalowu Sole, Chief Operating Officer, reported that the strong NS was helping generate revenues from fuel sales. Discussion followed as to whether the strong N$ was likely to persist and whether a strong N$ benefits Arrfield overall.

Markus Jokela. Chief Executive Officer, stated that the Board should develop contingency plans that could be implemented if it seemed likely that the strong N$ would persist. In particular. Arrfield need not renew the contracts that permit aviation fuel suppliers to operate from its airports. Arrfield would then be free to create its own fuel sale business, buying fuel in bulk to replenish the storage tanks at each of its airports in Norland and then selling it directly to airlines He stated that this would almost certainly enhance Arrfield's share price

Romuald Marek reminded the Board that four of Arrfield's six airports are located in Norland and that those airports charge for aeronautical and non-aeronautical services in N$.

Reference Material:

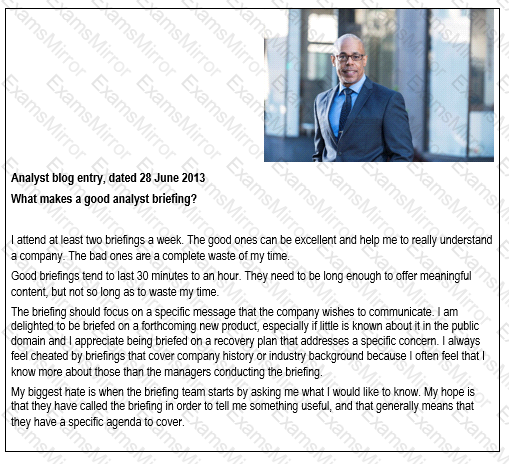

Wodd’s Chief Executive, Peter Sorchi has stopped you in the corridor:

"This weak USD is really causing us some serious problems. I think that it is only a matter of time before the stock market starts to get nervous and I am worried that our share price will fall in the near future. Thank goodness it does not appear to have fallen by much so far.

I would like to brief the Board on two main issues tomorrow. Firstly, what can we do as a Board in order to minimise the negative impact of the weak USD on our share price? Secondly, we know the identities of the key investment analysts who deal with our industry. Would it be a good idea for us to brief them? Please also consider the ethical issues arising from both of these topics as well as the more technical matters.

Please let me have a copy of your briefing notes in advance. I need to be able to sound convincing at the meeting. I’ll also have my secretary refer you to a really helpful blog."

Daily Gazette

Draft story for comment

The singer, the forester and the tax adviser

Popular singer Barry Crauder is regarded as one of our more financially-aware personalities. He works hard, releasing at least one new album every year and serving as a judge on a popular talent show. He has a reputation for investing this income wisely, choosing to save for his future rather than squandering on the trappings of the show business lifestyle.

Crauder’s popularity was severely damaged when it emerged that he pays little or no tax on the investment income derived from his portfolio of investments. That is because he has used one of the few remaining tax loopholes, namely investment in forestry. He owns significant areas of forestry in the far North of Marland. We estimate his earnings from those investments to exceed M$800,000 every year and yet he has not paid a single Cent in tax on that income since he first invested in forestry ten years ago. In contrast, a typical fan who earns the national average wage of M$28,000 every year will pay approximately M$7,000 in tax.

So, could we all invest in forestry? Well, not unless we can afford it. I posed as a wealthy business entrepreneur and approached several leading tax advisers. Most were interested in helping me to invest a seven figure sum to avoid tax, but warned that saving tax could be expensive in terms of fees and commissions.

Four firms recommended forestry as the ideal investment. All recommended Wodd, with whom all four claimed to conduct "significant business". They said that a typical client would give Wodd a bank draft and leave the purchase and subsequent management to Wodd in return for a fee. Most clients had never even seen the forests that they own and none ever need to make a management decision concerning the growth or sale of timber.

Sadly, investing in forestry is a rich person’s pursuit. I was warned that companies such as Wodd are unlikely to entertain a potential client whose initial investment does not run into the tens of millions of M$.

Please address any response to Sonia Jones, care of the Daily Gazette news desk, as quickly as possible.

From: Martin Wills, Head Geologist

To: William Seaton, Director of Finance

Subject: Reserves

Hi William,

I have reviewed the situation with respect to our “probable” or “2P” reserves, as disclosed in our latest annual report. I am sorry to say that we have to downgrade our figures with respect to reserves. I am recommending that all extraction activities cease for the foreseeable future on the North Atlantic and South Atlantic fields and that the proved reserves be downgraded from proved to probable.

I have to stress that this is not attributable to any past error on the part of the geologists. The world oil price has been depressed and the discovery of large deposits of shale oil in the USA suggests that the oil price will not recover for some time. That means that some oil wells that were commercially viable this time last year are no longer worth processing.

The oil remains under the rock and I have no doubt that we will restore operations in the long term.

We are by no means the only oil company to have been forced to take this action.

The one piece of good news is that the financial statements for the year ended 31 December 2014 have already been published. My understanding is that we do not have to withdraw them, so unless you put an advertisement in the press, we can carry on quietly trying to sort this mess out.

I have my best people working on ways to extract oil from our wells more efficiently, so we may be able to increase production over the next year or so.

Martin

The following email has just arrived:

From: William Seaton, Director of Finance

To: Finance Manager

Subject: News article

Hi,

My Secretary has drawn my attention to the attached newspaper clipping. I have been reading comments like this since Fouce Oil acquired its interest in 2010. We briefed the press at the time and made it clear that we would not be commenting further on our relationship with it unless it changed materially. Nothing has happened since then to make us change our mind on that.

The Board has asked me to compile a report on the following:

How might the presence of Fouce Oil, as a 25% shareholder, affect our decision making as a Board of Directors? Perhaps, surprisingly, we have never had a formal discussion of this matter.

How will Fouce Oil’s stake in Slide affect our share price?

I would like you to email me your thoughts on these points so that I can have as long as possible to think about what I will say to the Board.

Thanks

William

The newspaper clipping can be found by clicking on the Reference Materials button.

Memorandum of Understanding between Fouce Oil and Slide

It is proposed that Fouce Oil and Slide will temporarily combine their exploration activities, with Slide taking overall control in recognition of the greater expertise of its professional exploration staff.

This collaboration will work as follows:

1.Slide will take responsibility for the management and operation of all future exploration activities for the two companies, with effect from 1 October 2015.

2.Fouce Oil will second all of its professional oil exploration staff to Slide. Fouce will continue to employ these staff and will pay their salaries.

3.Slide will brief Fouce Oil’s professional oil exploration staff on all operational matters relating to exploration activities for the duration of this arrangement.

4.The provisions of paragraph 3 will apply to any projects in which Slide participates with third parties on a farm-in or other joint venture basis.

5.In recognition of Slide’s greater expertise, Fouce Oil will offer its entire portfolio of existing exploration rights to this venture, without any charge to Slide. Fouce Oil will also pay for 55% of any and all exploration costs, leaving Slide responsible for the remaining 45%.

6.The revenues from all successful discoveries will be shared equally by Slide and Fouce Oil. In the event that either party wishes to sell an oil well, the other will have the option of purchasing the other’s rights for 50% of the well’s agreed valuation.

7.This arrangement will be subject to review at the end of five years and annually thereafter. In the event that either party wishes to discontinue the arrangement, all ongoing exploration projects will be drawn to an orderly conclusion.

Signed

Thomas Yip, Chief Executive Officer, Fouce Oil

Andrew Jones, Chief Executive Officer, Slide

14 May 2015

Twelve hours have passed since you received the telephone call concerning the oil spillage.

You receive the following telephone call from William Seaton, Director of Finance:

“The press has got a hold of the story about the oil leak. Our share price has taken a major hit. Indeed, Slide’s market capitalisation has fallen by a third since the stock exchange opened for business. There is a lot of loose talk in the press about the knock-on effect of this crisis for Slide. It has not escaped anybody’s notice that there are news teams showing injured wildlife. There is also a great deal of footage being broadcast on the other sites around the world where we are revitalising oil wells using the same technology that was in use at AZ40.

Our experts have only just arrived at the spillage site. While they were on the corporate jet they emailed their initial thoughts, based on their understanding of what went wrong. Our engineers anticipate a major operation to block the leak by pumping cement into the bore hole at a low pressure. This will be expensive, but the cost will be less than one tenth of the reduction in our market capitalisation.

I need an email from you:

Firstly, I need a clear explanation of the key risks that Slide now faces because of this crisis. I am only interested in those with a high risk and high consequence and I need you to justify those classifications because the Board will need to prioritise its responses.

Secondly, two related issues: I need you to explain why Slide’s share price has fallen to such an extent AND to recommend, with reasons, whether we should release our costings of the repair scheme at this time.

It goes without saying that I need this urgently.”

Six months have passed since you briefed William Seaton, Director of Finance on the relationship between Slide and Fouce Oil.

You have been called into William Seaton’s office:

“We had a visit from the Chief Executive Officer of Fouce Oil yesterday. We had not received any prior notice of the purpose of the visit and assumed that he simply wished to make a courtesy call while he was visiting Fouce Oil’s subsidiary in this country. Instead, he came to initiate discussions over a strategy of collaboration on oil exploration.

Rather than explain things myself, please read the memorandum of understanding that he has asked us to sign. It is self-explanatory.

Once you have read the memorandum, I would like you to email me your thoughts on the following:

The suitability of this proposal for Slide.

The likelihood that Fouce Oil’s strategic interests will clash with our own.

The strategic risks that are likely to arise because of this arrangement.

The manner in which this strategic relationship should be communicated to the stock market.

I realise that this is a challenging request, but I need your response quickly because we need to respond to Fouce Oil.”

The Memorandum of Understanding can be found by clicking on the Reference Materials button.

TOP CODES

Top selling exam codes in the certification world, popular, in demand and updated to help you pass on the first try.