Summer Certification Limited Time 70% Discount Offer - Ends in 0d 00h 00m 00s - Coupon code = getmirror

Pass the PRMIA PRM Certification 8006 Questions and answers with ExamsMirror

Exam 8006 Premium Access

View all detail and faqs for the 8006 exam

789 Students Passed

97% Average Score

91% Same Questions

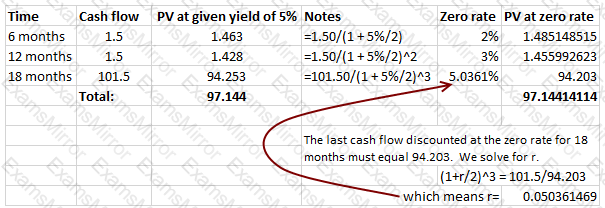

The yield offered by a bond with 18 months remaining to maturity is 5%. The coupon is 3%, paid semi-annually, and there are two more coupon payments to go in addition to the interest payment made at maturity. The zero rate for 6 months is 2%, that for 12 months is 3%. What is the 18 month zero rate?

If the 3 month interest rate is 5%, and the 6 month interest rate is 6%, what would be the contract rate applicable to a 3 x 6 FRA?

Assuming all other factors remain the same, an increase in the volatility of the returns on the assets of a firm causes which of the following outcomes?

For a deep in-the-money option:

A risk analyst working for an asset manager with a large debt portfolio is tasked with determining the suitability of using a traded debt ETF as a hedge against the value of the debt portfolio. He/she calculates the minimum variance hedge ratio to be exactly 1.0.

Given the above facts, which of the following statements are certainly true:

I. The ETF represents a perfect hedge for the portfolio

II. The volatility of the portfolio is the same as that for the ETF

III. The ETF cannot be used as an effective hedge for the debt portfolio

IV. None of the above

The forward price of a physical asset is affected by:

Which of the following statements are true:

I. A credit default swap provides exposure to credit risk alone and none to credit spreads

II. A CDS contract provides exposure to default risk and credit spreads

III. A TRS can be used as a funding source by the party paying LIBOR or other floating rate

IV. A CLN is an unfunded security for getting exposure to credit risk

The securities market line (SML) based upon the CAPM expresses the relationship between

Security A has a beta of 1.2 while security B has a beta of 1.5. If the risk free rate is 3%, and the expected total return from security A is 8%, what is the excess return expected from security B?

Euro-dollar deposits refer to

TOP CODES

Top selling exam codes in the certification world, popular, in demand and updated to help you pass on the first try.