Summer Certification Limited Time 70% Discount Offer - Ends in 0d 00h 00m 00s - Coupon code = getmirror

Pass the PRMIA PRM Certification 8010 Questions and answers with ExamsMirror

Exam 8010 Premium Access

View all detail and faqs for the 8010 exam

807 Students Passed

86% Average Score

90% Same Questions

Company A issues bonds with a face value of$100m, sold at $98. Bank B holds $10m in face of these bonds acquired at a price of $70. Company A then defaults, and the recovery rate is expected to be 30%. What is Bank B's loss?

Under the standardized approach to calculating operational risk capital under Basel II, negative regulatory capital charges for any of the business units:

For a bank using the advanced measurement approach to measuring operational risk, which of the following brings the greatest 'model risk' to its estimates:

Which of the following data sources are expected to influence operational risk capital under the AMA:

I. Internal Loss Data (ILD)

II. External Loss Data (ELD)

III. Scenario Data (SD)

IV. Business Environment and Internal Control Factors (BEICF)

Which of the following is not a parameter to be determined by the risk manager that affects the level of economic credit capital:

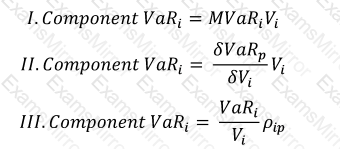

Which of the following formulae correctly describes Component VaR. (p refers to the portfolio, and i is the i-th constituent of the portfolio. MVaR means Marginal VaR, and other symbols have their usual meanings.)

When compared to a medium severity medium frequency risk, the operational risk capital requirement for a high severity very low frequency risk is likely to be:

Which of the following is NOT an approach used to allocate economic capital to underlying business units:

Which of the following statements is true:

I. Basel II requires banks to conduct stress testing in respect of their credit exposures in addition to stress testing for market risk exposures

II. Basel II requires pooled probabilities of default (and not individual PDs for each exposure) to be used for credit risk capital calculations

Under the KMV Moody's approach to credit risk measurement, how is the distance to default converted to expected default frequencies?

TOP CODES

Top selling exam codes in the certification world, popular, in demand and updated to help you pass on the first try.