Summer Certification Limited Time 70% Discount Offer - Ends in 0d 00h 00m 00s - Coupon code = getmirror

Pass the PRMIA PRM Certification 8013 Questions and answers with ExamsMirror

Exam 8013 Premium Access

View all detail and faqs for the 8013 exam

662 Students Passed

95% Average Score

98% Same Questions

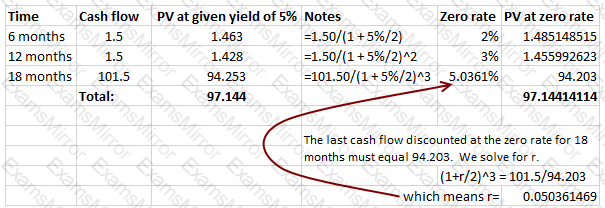

The yield offered by a bond with 18 months remaining to maturity is 5%. The coupon is 3%, paid semi-annually, and there are two more coupon payments to go in addition to the interest payment made at maturity. The zero rate for 6 months is 2%, that for 12 months is 3%. What is the 18 month zero rate?

If the exchange rate for USD/AUD is 0.6831 and the rate for SEK/USD is 8.1329, what is the SEK/AUD cross rate?

What kind of a risk attitude does a utility function with an upward sloping curvature indicate?

Basis risk between spot and futures prices tends to be the highest for:

Suppose the S&P is trading at a level of 1000. Using continuously compounded rates, calculate the futures price for a contract expiring in three months, assuming expected dividends to be 2% and the interest rate for futures funding to be 5% (both rates expressed as continuously compounded rates)

Calculate the net payment due on a fixed-for-floating interest rate swap where the fixed rate is 5% and the floating rate is LIBOR + 100 basis points. Assume reset dates are every six months, LIBOR at the beginning of the reset period is 4.5% and at the end of the period is 3.5%. Notional is $1m.

An investor expects stock prices to move either sharply up or down. His preferred strategy should be to:

A normal yield curve is generally:

What would be the expected return on a stock with a beta of 1.2, when the risk free rate is 3% and the broad market index is expected to earn 8%?

A corn farmer has committed to sell 20,000 bushels of corn in November. The spot price has a standard deviation of 20 cents per bushel, and its correlation with the December futures prices is 0.9. The futures contract is for 5000 bushels and has a standard deviation of 24 cents per bushel. What should the corn producer do if he/she wishes to hedge the risk of price movements between now and November?

TOP CODES

Top selling exam codes in the certification world, popular, in demand and updated to help you pass on the first try.