Summer Certification Limited Time 70% Discount Offer - Ends in 0d 00h 00m 00s - Coupon code = getmirror

Pass the PRMIA PRM Certification 8008 Questions and answers with ExamsMirror

Exam 8008 Premium Access

View all detail and faqs for the 8008 exam

670 Students Passed

96% Average Score

91% Same Questions

Which of the following are ordered correctly in the order of debt seniority in a bankruptcy situation?

I. Equity, Subordinate debt, Senior debt

II. Senior debt, Preferred stock, Equity

III. Secured debt, Accounts payable, Preferred stock

IV. Secured debt, DIP financing, Equity

Which of the following cannot be used to address the issue of heavy tails when modeling market returns

Under the actuarial (or CreditRisk+) based modeling of defaults, what is the probability of 4 defaults in a retail portfolio where the number of expected defaults is 2?

Which of the following statements is correct in relation to liquidity risk management?

I. Pricing for products that do not impact the balance sheet need not reflect the cost of maintaining liquidity

II. Time horizons for liquidity risk management are impacted by both regulatory requirements and the speed at which new sources of liquidity can be tapped

III. Collateral management is an important aspect of liquidity risk management

IV. The maturity period of various instruments in the capital structure has a significant impact on liquidity needs

For a US based investor, what is the 10-day value-at risk at the 95% confidence level of a long spot position of EUR 15m, where the volatility of the underlying exchange rate is 16% annually. The current spot rate for EUR is 1.5. (Assume 250 trading days in a year).

The capital adequacy ratio applied to risk weighted assets for the calculation of capital requirements for credit risk per Basel II is:

Financial institutions need to take volatility clustering into account:

I. To avoid taking on an undesirable level of risk

II. To know the right level of capital they need to hold

III. To meet regulatory requirements

IV. To account for mean reversion in returns

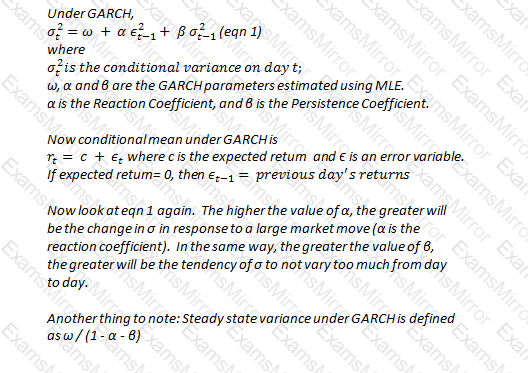

What is the annualized steady state volatility under a GARCH model where alpha is 0.1, beta is 0.8 and omega is 0.00025?

The systemic manifestation of the liquidity crisis during the current credit crisis took many forms. Which of the following is not one of those forms?

Which of the following formulae describes CVA (Credit Valuation Adjustment)? All acronyms have their usual meanings (LGD=Loss Given Default, ENE=Expected Negative Exposure, EE=Expected Exposure, PD=Probability of Default, EPE=Expected Positive Exposure, PFE=Potential Future Exposure)

TOP CODES

Top selling exam codes in the certification world, popular, in demand and updated to help you pass on the first try.