Summer Certification Limited Time 70% Discount Offer - Ends in 0d 00h 00m 00s - Coupon code = getmirror

Pass the PRMIA PRM Certification 8008 Questions and answers with ExamsMirror

Exam 8008 Premium Access

View all detail and faqs for the 8008 exam

670 Students Passed

96% Average Score

91% Same Questions

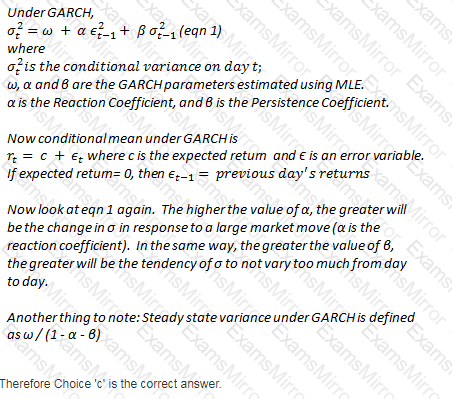

As the persistence parameter under GARCH is lowered, which of the following would be true:

What would be the consequences of a model of economic risk capital calculation that weighs all loans equally regardless of the credit rating of the counterparty?

I. Create an incentive to lend to the riskiest borrowers

II. Create an incentive to lend to the safest borrowers

III. Overstate economic capital requirements

IV. Understate economic capital requirements

Which of the following statements are true with respect to stress testing:

I. Stress testing results in a dollar estimate of losses

II. The results of stress testing can replace VaR as a measure of risk as they are better grounded in reality

III. Stress testing provides an estimate of losses at a desired level of confidence

IV. Stress testing based on factor shocks can allow modeling extreme events that have not occurred in the past

Identify the correct sequence of events as it unfolded in the credit crisis beginning 2007:

I. Mortgage defaults increased

II. Collapse in prices of unrelated assets as banks tried to create liquidity

III. Banks refused to lend or transact with each other

IV. Asset prices for CDOs collapsed

In respect of operational risk capital calculations, the Basel II accord recommends a confidence level and time horizon of:

Which of the following objectives are targeted by rating agencies when assigning ratings:

I. Ratings accuracy

II. Ratings stability

III. High accuracy ratio (AR)

IV. Ranked ratings

If the full notional value of a debt portfolio is $100m, its expected value in a year is $85m, and the worst value of the portfolio in one year's time at 99% confidence level is $60m, then what is the credit VaR?

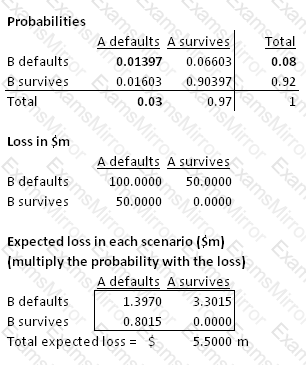

There are two bonds in a portfolio, each with a market value of $50m. The probability of default of the two bonds are 0.03 and 0.08 respectively, over a one year horizon. If the default correlation is 25%, what is the one year expected loss on this portfolio?

Which of the following statements is true:

I. Basel II requires banks to conduct stress testing in respect of their credit exposures in addition to stress testing for market risk exposures

II. Basel II requires pooled probabilities of default (and not individual PDs for each exposure) to be used for credit risk capital calculations

Altman's Z-score does not consider which of the following ratios:

TOP CODES

Top selling exam codes in the certification world, popular, in demand and updated to help you pass on the first try.