Summer Certification Limited Time 70% Discount Offer - Ends in 0d 00h 00m 00s - Coupon code = getmirror

Pass the PRMIA PRM Certification 8008 Questions and answers with ExamsMirror

Exam 8008 Premium Access

View all detail and faqs for the 8008 exam

670 Students Passed

96% Average Score

91% Same Questions

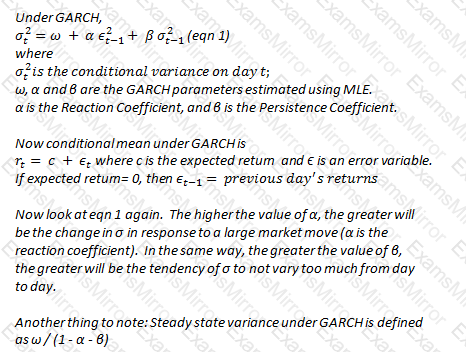

A risk analyst uses the GARCH model to forecast volatility, and the parameters he uses are ω = 0.001%, α = 0.05 and β = 0.93. Yesterday's daily volatility was calculated to be 1%. What is the long term annual volatility under the analyst's model?

Under the internal ratings based approach for risk weighted assets, for which of the following parameters must each institution make internal estimates (as opposed to relying upon values determined by a national supervisor):

For an investor with a long position in market index futures, which of the following is a primary risk:

If the default hazard rate for a company is 10%, and the spread on its bonds over the risk free rate is 800 bps, what is the expected recovery rate?

Which of the following statements are true:

I. Top down approaches help focus management attention on the frequency and severity of loss events, while bottom up approaches do not.

II. Top down approaches rely upon high level data while bottom up approaches need firm specific risk data to estimate risk.

III. Scenario analysis can help capture both qualitative and quantitative dimensions of operational risk.

A stock that follows the Weiner process has its future price determined by:

If the 99% VaR of a portfolio is $82,000, what is the value of a single standard deviation move in the portfolio?

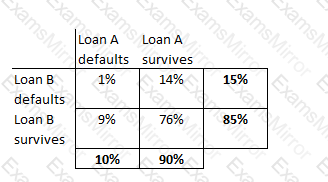

A portfolio has two loans, A and B, each worth $1m. The probability of default of loan A is 10% and that of loan B is 15%. The probability of both loans defaulting together is 1%. Calculate the expected loss on the portfolio.

Which of the following does not affect the credit risk facing a lender institution?

An error by a third party service provider results in a loss to a client that the bank has to make up. Such as loss would be categorized per Basel II operational risk categories as:

TOP CODES

Top selling exam codes in the certification world, popular, in demand and updated to help you pass on the first try.