Summer Certification Limited Time 70% Discount Offer - Ends in 0d 00h 00m 00s - Coupon code = getmirror

Pass the PRMIA PRM Certification 8008 Questions and answers with ExamsMirror

Exam 8008 Premium Access

View all detail and faqs for the 8008 exam

670 Students Passed

96% Average Score

91% Same Questions

Which of the following statements is true in relation to a normal mixture distribution:

I. The mixture will always have a kurtosis greater than a normal distribution with the same mean and variance

II. A normal mixture density function is derived by summing two or more normal distributions

III. VaR estimates for normal mixtures can be calculated using a closed form analytic formula

Economic capital under the Earnings Volatility approach is calculated as:

Credit exposure for derivatives is measured using

For the purposes of calculating VaR, an interest rate swap can be modeled as a combination of:

For a back office function processing 15,000 transactions a day with an error rate of 10 basis points, what is the annual expected loss frequency (assume 250 days in a year)

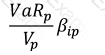

Which of the following formulae describes Marginal VaR for a portfolio p, where V_i is the value of the i-th asset in the portfolio? (All other notation and symbols have their usual meaning.)

A)

B)

C)

D)

All of the above

Which of the following are elements of 'group risk':

I. Market risk

II. Intra-group exposures

III. Reputational contagion

IV. Complex group structures

Which of the following statements is true?

I. It is sufficient to ensure that a parent entity has sufficient excess liquidity to cover a liquidity shortfall for a subsidiary.

II. If a parent entity has a shortfall of liquidity, it can always rely upon any excess liquidity that its foreign subsidiaries might have.

III. Wholesale funding sources for a bank refer to stable sources of funding provided by the central bank.

IV. Funding diversification refers to diversification of both funding sources and funding tenors.

Under the basic indicator approach to determining operational risk capital, operational risk capital is equal to:

A risk management function is best organized as:

TOP CODES

Top selling exam codes in the certification world, popular, in demand and updated to help you pass on the first try.