Summer Certification Limited Time 70% Discount Offer - Ends in 0d 00h 00m 00s - Coupon code = getmirror

Pass the PRMIA PRM Certification 8011 Questions and answers with ExamsMirror

Exam 8011 Premium Access

View all detail and faqs for the 8011 exam

705 Students Passed

97% Average Score

94% Same Questions

A stock that follows the Weiner process has its future price determined by:

Which of the following are attributes of a robust stress testing programme at a bank?

Which of the following is NOT true in respect of bilateral close out netting:

Which of the following statements is true:

I. Recovery rate assumptions can be easily made fairly accurately given past data available fromcredit rating agencies.

II. Recovery rate assumptions are difficult to make given the effect of the business cycle, nature of the industry and multiple other factors difficult to model.

III. The standard deviation of observed recovery rates is generally very high, making any estimate likely to differ significantly from realized recovery rates.

IV. Estimation errors for recovery rates are not a concern as they are not directionally biased and will cancel each other out over time.

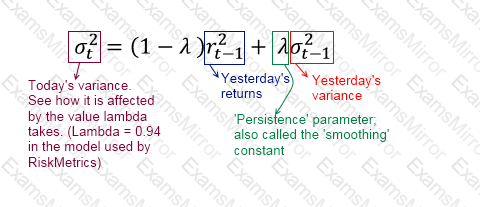

A stock's volatility under EWMA is estimated at 3.5% on a day its price is $10. The next day, the price moves to $11. What is the EWMA estimate of the volatility the next day? Assume the persistence parameter λ = 0.93.

A diagram of a mathematical equation

Description automatically generated

A diagram of a mathematical equation

Description automatically generatedWhich of the following is not a limitation of the univariate Gaussian model to capture the codependence structure between risk factros used for VaR calculations?

Which of the following are valid criticisms of value at risk:

I. There are many risks that a VaR framework cannot model

II. VaR does not consider liquidity risk

III. VaR does not account for historical market movements

IV. VaR does not consider the risk of contagion

Which of the following will be a loss not covered by operational risk as defined under Basel II?

The VaR of a portfolio at the 99% confidence level is $250,000 when mean return is assumed to be zero. If the assumption of zero returns is changed to an assumption of returns of $10,000, what is the revised VaR?

Which of the following statements are true:

I. Credit VaR often assumes a one year time horizon, as opposed to a shorter time horizon for market risk as credit activities generally span a longer time period.

II. Credit losses in the banking book should be assessed on the basis of mark-to-market mode as opposed to the default-only mode.

III. The confidence level used in the calculation of credit capital is high when the objective is to maintain a high credit rating for the institution.

IV. Credit capital calculations for securities with liquid markets and held for proprietary positions should be based on marking positions to market.

TOP CODES

Top selling exam codes in the certification world, popular, in demand and updated to help you pass on the first try.