Summer Certification Limited Time 70% Discount Offer - Ends in 0d 00h 00m 00s - Coupon code = getmirror

Pass the PRMIA PRM Certification 8011 Questions and answers with ExamsMirror

Exam 8011 Premium Access

View all detail and faqs for the 8011 exam

705 Students Passed

97% Average Score

94% Same Questions

Which of the following statements are true with respect to stress testing:

I. Stress testing results in a dollar estimate of losses

II. The results of stress testing can replace VaR as a measure of risk as they are better grounded in reality

III. Stress testing provides an estimate of losses at a desired level of confidence

IV. Stress testing based on factor shocks can allow modeling extreme events that have not occurred in the past

Which of the following is the best description of the spread premium puzzle:

Which of the following statements are true in relation to Historical Simulation VaR?

I. Historical Simulation VaR assumes returns are normally distributed but have fat tails

II. It uses full revaluation, as opposed to delta or delta-gamma approximations

III. A correlation matrix is constructed using historical scenarios

IV. It particularly suits new products that may not have a long time series of historical data available

Which of the following are valid objectives of a reverse stress test:

I. Ensure that a firm can survive for long enough after risks have materialized for it to either regainmarket confidence, restructure or be sold, or be closed down in an orderly manner,

II. Discover the vulnerabilities of the current business plan,

III. Better integrate business and capital planning,

IV. Create a 'zero-failure' environment at the systemic level in the financial sector

In setting confidence levels for VaR estimates for internal limit setting, it is generally desirable:

A risk analyst analyzing the positions for a proprietary trading desk determines that the combined annual variance of the desk's positions is 0.16. The value of the portfolio is $240m. What is the 10-day stand alone VaR in dollars for the desk at a confidence level of 95%? Assume 250 trading days in a year.

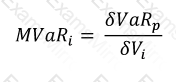

Which of the following best describes the concept of marginal VaR of an asset in a portfolio:

A mathematical equation with numbers and symbols

Description automatically generated

A mathematical equation with numbers and symbols

Description automatically generatedWhen modeling operational risk using separate distributions for loss frequency and loss severity, which of the following is true?

An assumption of normality when returns data have fat tails leads to:

I. underestimation of VaR at high confidence levels

II. overestimation of VaR at low confidence levels

III. overestimation of VaR at high confidence levels

IV. underestimation of VaR at low confidence levels

Which of the following is not an event of default covered in the ISDA Master Agreement?

I. failure to pay or deliver

II. credit support default

III. merger without assumption

IV. Bankruptcy

TOP CODES

Top selling exam codes in the certification world, popular, in demand and updated to help you pass on the first try.