Summer Certification Limited Time 70% Discount Offer - Ends in 0d 00h 00m 00s - Coupon code = getmirror

Pass the PRMIA PRM Certification 8011 Questions and answers with ExamsMirror

Exam 8011 Premium Access

View all detail and faqs for the 8011 exam

705 Students Passed

97% Average Score

94% Same Questions

A bank holds a portfolio of corporate bonds. Corporate bond spreads widen, resulting in a loss of value for the portfolio. This loss arises due to:

Which of the following statements is true:

Which of the following statements are true:

I. The sum of unexpected losses for individual loans in a portfolio is equal to the total unexpected loss for the portfolio.

II. The sum of unexpected losses for individual loans in a portfolio is less than the total unexpected loss for the portfolio.

III. The sum of unexpected losses for individual loans in a portfolio is greater than the total unexpected loss for the portfolio.

IV. The unexpected loss for the portfolio is driven by the unexpected losses of the individual loans in the portfolio and the default correlation between these loans.

The largest 10 losses over a 250 day observation period are as follows. Calculate the expected shortfall at a 98% confidence level:

20m

19m

19m

17m

16m

13m

11m

10m

9m

9m

An investor enters into a 5-year total return swap with Bank A, with the investor paying a fixed rate of 6% annually on a notional value of $100m to the bank and receiving the returns of the S&P500 index with an identical notional value. The swap is reset monthly, ie the payments are exchanged monthly. On Jan 1 of the fourth year, after settling the last month's payments, the bank enters bankruptcy. What is the legal claim that the hedge fund has against the bank in the bankruptcy court?

Once the frequency and severity distributions for loss events have been determined, which of the following is an accurate description of the process to determine a full loss distribution foroperational risk?

Which of the following correctly describes survivorship bias:

Which of the following are considered properties of a 'coherent' risk measure:

I. Monotonicity

II. Homogeneity

III. Translation Invariance

IV. Sub-additivity

If the duration of a bond yielding 10% is 6 years, the volatility of the underlying interest rates 5% per annum, what is the 10-day VaR at 99% confidence of a bond position comprising just this bond with a value of $10m? Assume there are 250 days in a year.

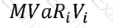

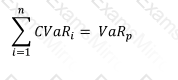

Which of the formulae below describes incremental VaR where a new position 'm' is added to the portfolio? (where p is the portfolio, and V_i is the value of the i-th asset in the portfolio. All other notation and symbols have their usual meaning.)

A)

B)

C)

D)

TOP CODES

Top selling exam codes in the certification world, popular, in demand and updated to help you pass on the first try.