Summer Certification Limited Time 70% Discount Offer - Ends in 0d 00h 00m 00s - Coupon code = getmirror

Pass the PRMIA PRM Certification 8011 Questions and answers with ExamsMirror

Exam 8011 Premium Access

View all detail and faqs for the 8011 exam

705 Students Passed

97% Average Score

94% Same Questions

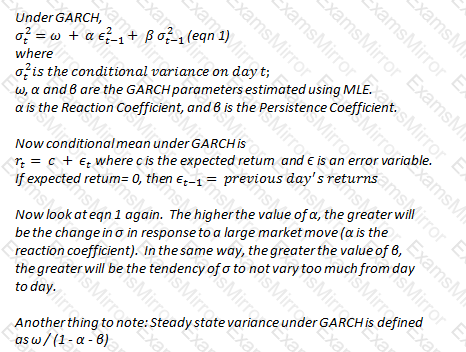

A risk analyst uses the GARCH model to forecast volatility, and the parameters he uses are ω = 0.001%, α = 0.05 and β = 0.93. Yesterday's daily volatility was calculated to be 1%. What is the long term annual volatility under the analyst's model?

A white text with black text

Description automatically generated

A white text with black text

Description automatically generatedA bank prices retail credit loans based on median default rates. Over the long run, it can expect:

Under the KMV Moody's approach to calculating expecting default frequencies (EDF), firms' default on obligations is likely when:

CreditRisk+, the actuarial model for calculating portfolio credit risk, is based upon:

Which of the following cannot be used as an internal credit rating model to assess an individual borrower:

Which of the following are likely to be useful to a risk manager analyzing liquidity risk for an international bank?

I. Information on liquidity mismatches

II. Funding concentration

III. Lending concentration

IV. A report on illiquid assets

Under the standardized approach to calculating operational risk capital under Basel II, negative regulatory capital charges for any of the business units:

Which of the following statements are correct:

I. A training set is a set of data used to create a model, while a control set is a set of data is used to prove that the model actually works

II. Cleansing, aggregating or ensuring data integrity is a task for the IT department, and is not a risk manager's responsibility

III. Lack of information on the quality of underlying securities and assets was a major cause of the collapse in the CDO markets during the credit crisis that started in 2007

IV. The problem of lack of historical data can be addressed reasonably satisfactorily by using analytical approaches

For a corporate issuer, which of the following can be used to calculate market implied default probabilities?

I. CDS spreads

II. Bond prices

III. Credit rating issued by S&P

IV. Altman's scoring model

Which of the following are true:

I. The total of the component VaRs for all components of a portfolio equals the portfolio VaR.

II. The total of the incremental VaRs for each position in a portfolio equals the portfolio VaR.

III. Marginal VaR and incremental VaR are identical for a $1 change in the portfolio.

IV. The VaR for individual components of a portfolio is sub-additive, ie the portfolio VaR is less than (or in extreme cases equal to) the sum of the individual VaRs.

V. The component VaR for individual components of a portfolio is sub-additive, ie the portfolio VaR is less than the sum of the individual component VaRs.

TOP CODES

Top selling exam codes in the certification world, popular, in demand and updated to help you pass on the first try.