Summer Certification Limited Time 70% Discount Offer - Ends in 0d 00h 00m 00s - Coupon code = getmirror

Pass the PRMIA PRM Certification 8011 Questions and answers with ExamsMirror

Exam 8011 Premium Access

View all detail and faqs for the 8011 exam

705 Students Passed

97% Average Score

94% Same Questions

An asset has a volatility of 10% per year. An investment manager chooses to hedge it with another asset that has a volatility of 9% per year and a correlation of 0.9. Calculate the hedge ratio.

For an option position with a delta of 0.3, calculate VaR if the VaR of the underlying is $100.

An equity manager holds a portfolio valued at $10m which has a beta of 1.1. He believes the market may see a dip in the coming weeks and wishes to eliminate his market exposure temporarily. Market index futures are available and the current futures notional on these is $50,000 per contract. Which of the following represents the best strategy for the manager to hedge his risk according to his views?

When performing portfolio stress tests using hypothetical scenarios, which of the following is not generally a challenge for the risk manager?

Which of the following should be included when calculating the Gross Income indicator used to calculate operational risk capital under the basic indicator and standardized approaches under Basel II?

If A and B be two debt securities, which of the following is true?

A black line with letters and numbers

Description automatically generated

A black line with letters and numbers

Description automatically generatedFor a security with a daily standard deviation of 2%, calculate the 10-day VaR at the 95% confidence level. Assume expected daily returns to be nil.

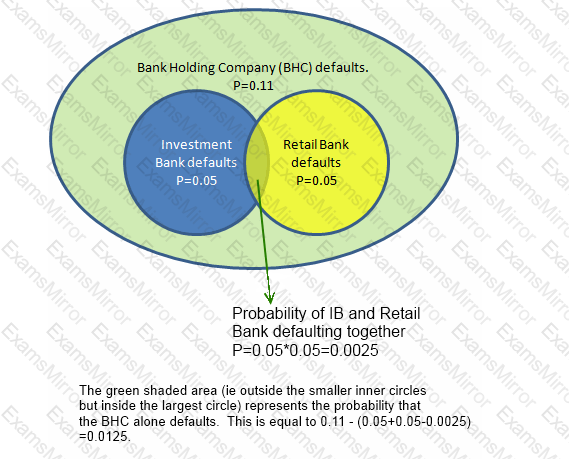

A Bank Holding Company (BHC) is invested in an investment bank and a retail bank. The BHC defaults for certain if either the investment bank or the retail bank defaults. However, the BHC can also default on its own without either the investment bank or the retail bank defaulting. The investment bank and the retail bank's defaults are independent of each other, with a probability of default of 0.05 each. The BHC's probability of default is 0.11.

What is the probability of default of both the BHC and the investment bank? What is the probability of the BHC's default provided both the investment bank and the retail bank survive?

A diagram of a bank

Description automatically generated

A diagram of a bank

Description automatically generatedWhich of the following statements is correct in relation to liquidity risk management?

I. Pricing for products that do not impact the balance sheet need not reflect the cost of maintaining liquidity

II. Time horizons for liquidity risk management are impacted by both regulatory requirements and the speed at which new sources of liquidity can be tapped

III. Collateral management is an important aspect of liquidity risk management

IV. The maturity period of various instruments in the capital structure has a significant impact on liquidity needs

Calculate the 1-year 99% credit VaR of a portfolio of two bonds, each with a value of $1m, and the probability of default of 1% each over the next year. Assume the recovery rate to be zero, and the defaults of the two bonds to be uncorrelated to each other.

TOP CODES

Top selling exam codes in the certification world, popular, in demand and updated to help you pass on the first try.